Mortgage assistance programs offer hope to veterans and service members struggling to make monthly mortgage payments due to unexpected circumstances like medical expenses, job loss, or financial downturns.

These programs encompass various solutions, such as forbearance agreements, loan modifications, and refinancing opportunities. They reduce the economic burden and make mortgage obligations more manageable.

Veteran mortgage assistance programs, like VA loans, are supported by the United States Department of Veterans Affairs (VA). They help veterans, military active-duty personnel, and other groups become homeowners at affordable costs.

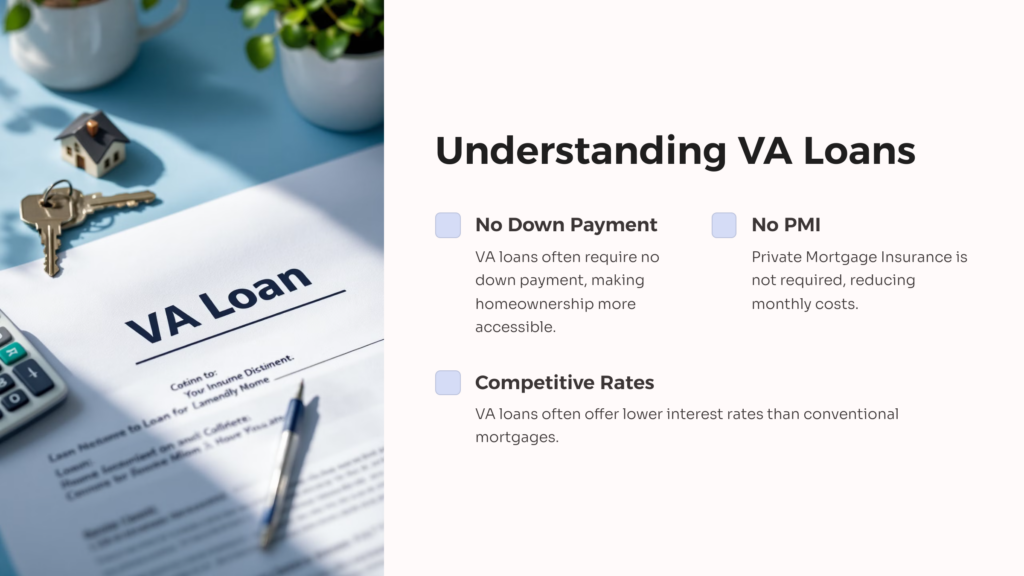

One critical benefit of VA loans is their accessibility. They require no PMI (private mortgage insurance) or down payment, and their eligibility rules are designed to be lenient, ensuring that a wide range of individuals, including veterans and military active-duty personnel, can benefit from them.

Understanding Veteran Mortgage Assistance

Veteran mortgage assistance includes VA mortgage loans, which are available through programs established by the VA. With veteran mortgage assistance, veterans and their surviving spouses can buy homes with no private mortgage insurance and little to no down payment and even secure competitive interest rates.

VA grants and loans usually don’t require a down payment, but you still need sufficient income and a decent credit score to get approved.

VA mortgage assistance programs have helped many veterans and their surviving spouses refinance or buy homes. You’re eligible to apply for a VA mortgage assistance program if:

- You’re on active duty and have served three continuous months in the military.

- You’re a veteran who has served 90 days in wartime and at least 181 days in peacetime.

- You have completed three months of active duty or six years in the National Guard or Selected Reserve.

- You’re a qualifying surviving spouse of a military veteran who died from a service-related disability or while on service and has not remarried. Or you married after Dec. 16, 2003, or at age 57. Also, spouses of prisoners of war or service members missing in action are eligible for veteran mortgage assistance.

You can still qualify for VA mortgage assistance even though you don’t meet the length-of-service conditions in some instances, like being discharged from military service because of a service-related disability.

However, you may not qualify for VA home loans and grants if you received an “other than honorable,” dishonorable discharge or bad conduct, even though you can apply with the Department of Veterans Affairs to upgrade your discharge status.

Benefits of Veteran Mortgage Assistance

Suppose you’re an eligible veteran, active-duty military member, or surviving spouse. In that case, you can use veteran mortgage assistance solutions like grants and home loans to buy new property or refinance an existing mortgage. There are many other benefits of these solutions, including:

- Lower interest rates. Banks and other lenders often charge lower interest rates for VA mortgage assistance programs than they do on conventional mortgage options, which means you’ll save tons of money on interest rates and fees in the long run, especially for a 20-year mortgage loan. Further, VA mortgage loan closing expenses might be less than those for other conventional home loans because the VA limits the origination fees lenders can levy to no more than 1% of the mortgage.

- No down payment. Although conventional mortgages necessitate a down payment of 4% of the purchase price, VA grants and loans enable eligible borrowers to own homes without putting a penny down in advance. This makes a significant difference: 40% of Americans who don’t own homes cite closing costs and inability to pay a down payment as the primary reason for continuing to rent.

- Reusing the benefits. You can reuse VA mortgage assistance over and over again. Homeowners often regain the full power of their benefits after selling a house and repaying the original mortgage in full. Also, it’s possible to buy a home with veteran mortgage assistance, live in it for a while, rent it out, and purchase a new house using the remaining VA mortgage entitlement. You must sell a house to regain your full veteran mortgage entitlement. The VA offers all eligible buyers an opportunity to repay a veteran mortgage in full, keep the home, and buy again with their full entitlement.

- Lifetime benefit for veterans. Veterans eligible for veteran mortgage assistance can use this program forever, and the benefits never expire. In fact, you don’t have to repay your VA home loan to use your benefits again. Having more than one VA home loan simultaneously with second-tier entitlement is possible.

Veteran Mortgage Assistance Programs

VA loans and grants are among the most powerful mortgage options for active military personnel, veterans, and surviving spouses. The power behind veteran mortgage assistance programs comes from significant financial benefits not found in conventional mortgage options. Common Veteran mortgage assistance programs include:

Home Loans by Veterans Affairs (VA)

VA home loans are one of the most potent military benefits. If you’re eligible for this type of loan, you can refinance an existing home mortgage or buy or build a new home with excellent financing and interest rates with no mandated cap. A VA home loan makes buying a home more affordable for millions of active service members and veterans. To qualify for a VA home loan, you must have served on active duty in the military for at least three months or meet other military service benchmarks for Reserve and Guard members.

The Native American Direct Loan Program

The Native American Direct Loan (NADL) program helps Native Americans build, buy, refinance, or improve properties on federal trust land. It is available to members of some Native American tribes and their surviving spouses, residents of Pacific Island territories, and Alaska Native corporations.

To access this program, check if your native community participates in the Native American Direct Loan program, then apply for a Veteran Affairs (VA) COE (certificate of eligibility) and contact the VA regional loan office in your state.

Adapted Housing Grants

The VA offers adapted housing grants to veterans and service members suffering from specific service-related disabilities so they can modify or buy a home that meets their needs and live more comfortably. Modifying a home may involve widening doorways or installing ramps. You might be able to get an adapted housing grant if you plan to buy, build, or modify your permanent home and you meet these requirements:

- You will own or own the home, and

- You have a rated service-related disability.

Interest Rate Reduction Refinance Loan (IRRRL)

A VA streamline refinance, also referred to as an IRRRL, helps veterans lower their interest rates by refinancing existing VA loans. This program allows borrowers with existing VA loans to convert adjustable-rate mortgages into fixed-rate mortgages or refinance fixed-rate loans at low-interest rates. VA IRRRL loans are available only to veterans with active VA loans.

Application Process for Veteran Mortgage Assistance Programs

You can apply for veteran mortgage assistance through a mortgage company, bank, or credit union. The process is similar to when applying for other types of mortgages: you simply supply income, employment, and other financial details, and the lender determines if you qualify for a VA loan.

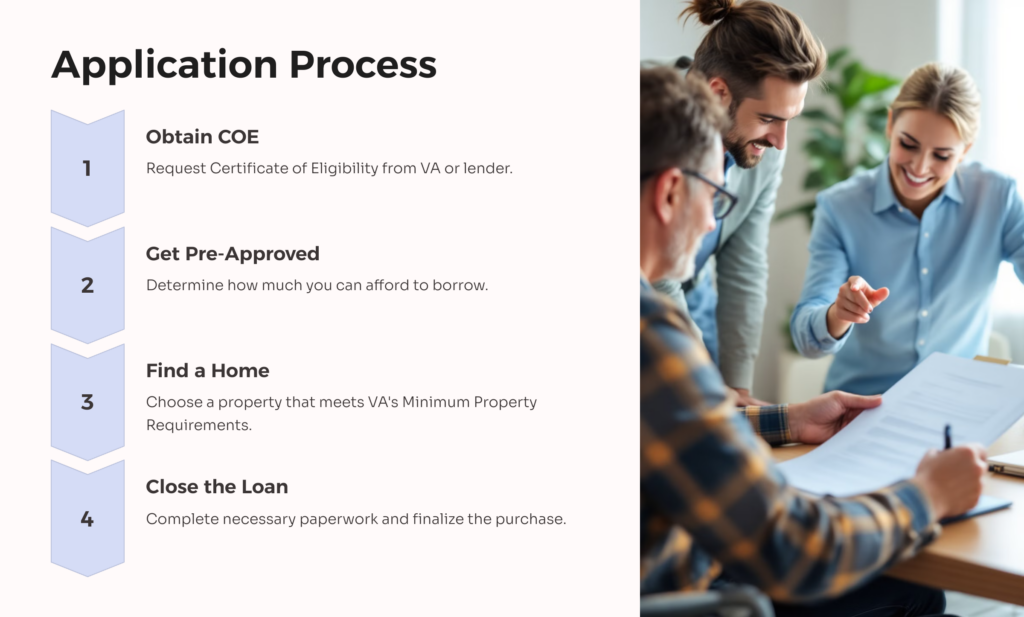

One crucial document you’ll require when applying for veteran mortgage assistance is a VA certificate of eligibility (COE). The COE shows that you meet the service requirements for veteran mortgage assistance. You can request this document from the VA or ask your VA mortgage lender to get it.

When purchasing a home, you must also get pre-approved in advance. The approval is a baseline for gauging how much you can afford. Besides, when you make an offer on a home, you’ll realize that sellers often take offers seriously if a preapproval letter is attached.

Next, shop for a home. Finding a home with veteran mortgage assistance is like finding a home with any other mortgage option. The house you buy must meet the MPRs (VA’s Minimum Property Requirements), which ensure a property is sanitary, structurally sound, and safe. After you find a property within your price range, make an offer to buy the house.

Lenders will then review your debt, credit, and income to determine if you qualify for veteran mortgage assistance and the interest rates they offer. The VA hasn’t set a minimum credit score to qualify for mortgage assistance. However, other VA mortgage lenders may have their own minimum requirements for FICO credit scores, often in the low—to mid-600s.

The VA requires a debt-to-income ratio of no more than 41%. However, veterans with higher ratios can be approved for VA loans and grants if they have adequate “residual income,” another crucial factor lenders consider when reviewing VA mortgage applications. Residual income that covers basic living expenses like clothing and food after covering housing, debts, and other financial obligations.

Often, VA mortgage assistance programs don’t require a minimum down payment. But if the purchase price of a house is more than its appraised value, you might have to make up a percentage of the difference.

Further, you must make a down payment if you’re subject to VA loan limits and the house price exceeds county loan limits.

Tips for Navigating the Veteran Mortgage Assistance Programs

Owning a home can be challenging, especially for veterans. But with the right resources and guidance, securing a mortgage can be more manageable. At AllVeteran, we know the unique challenges veterans may face while navigating the housing market. That’s why we’ve curated tips to help you secure veteran mortgage assistance smoothly.

Leveraging VA Loans and Grants Benefits

One of the fundamental benefits of VA loans and grants is their affordability and flexibility. As a veteran, you can avoid private mortgage insurance and secure favorable interest rates, leading to significant savings. Further, VA mortgage assistance programs often have low credit score requirements compared to other mortgages, making them more accessible to a wide range of borrowers.

Working with Experienced Professionals

Navigating the mortgage process is daunting, especially if you’re unfamiliar with the intricacies of VA grants and loans. Thus, working with experienced and knowledgeable lenders is essential. Knowledgeable professionals can help you navigate the complicated mortgage process, ensuring you make educated decisions and secure the most favorable terms.

Preparing for the Mortgage Application Process

Gathering all vital documents before applying for VA mortgage assistance is crucial to streamlining the application process. This includes income verification documentation, proof of military service, and information about your current financial circumstances. Gathering this documentation in advance can expedite the mortgage application process, increasing your approval odds.

Exploring Additional Resources

Besides VA loans, veterans might qualify for other housing assistance grants and programs. These additional resources can help you cover down payments, closing costs, and renovations to accommodate disabilities. By exploring the available options, you can maximize your benefits and achieve your homeownership goals efficiently.

Real Stories of Veterans Benefiting from Mortgage Assistance

VA purchase loans have helped many service members, veterans, and eligible military spouses refinance or buy homes. Those who secure these loans don’t have to put any cash down and aren’t required to secure private mortgage insurance–a significant help to most young homebuyers.

For instance, Eddie Valdivia and his wife bought their first home in 2020 thanks to VA purchase loans. Eddie is a military veteran who served in the Navy for over eight years, so he secured a VA purchase loan, which helped him buy the home without a down payment.

VA mortgage assistance programs have also helped other veterans like Isis Frasier become homeowners. Thanks to VA purchase loans, Isis, a veteran, could buy the home of her dreams with no money down and a lower credit score.

These are just a few examples of veterans and their families using their veterans benefits to purchase homes, even with low credit scores and no money down.

Conclusion: Veteran Mortgage Assistance

VA mortgage assistance programs, like VA home loans and adapted housing grants, are top benefits for eligible service members, veterans, and qualifying surviving spouses. You’ll get favorable interest rates if you’re eligible for these benefits. That means homeownership is more affordable with veteran mortgage assistance programs.

AllVeteran.com Advisors

AllVeteran.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.