VA cash out refinance is a mortgage option that allows eligible veterans to refinance their existing mortgage payment while simultaneously withdrawing cash from their home’s equity. This unique feature distinguishes it from other types of refinancing, such as the VA Interest Rate Reduction Refinance Loan (IRRRL), by providing veterans with a source of funds for various purposes. Qualifying veterans must have a VA loan, and the new loan must be larger than the existing one.

Benefits of VA Cash-Out Refinance for Veterans

Veterans exploring financial options will find that VA cash out refinance offers many advantages, providing a unique avenue for leveraging the equity in their homes. This financial tool not only facilitates the reduction of your monthly mortgage payment but also grants access to funds for various purposes, enhancing veterans’ financial flexibility and well-being.

Home Improvements

VA cash-out refinance empowers veterans to enhance the value and comfort of their homes. Whether renovating a kitchen, upgrading a bathroom, or making essential structural repairs, veterans can use the released equity to invest in their property, ultimately increasing its market value.

Debt Consolidation

For veterans carrying multiple high-interest debts, VA cash-out refinance provides an opportunity to consolidate debts into a single, more manageable mortgage. This simplifies financial management and can result in lower overall interest rates, saving veterans money in the long run.

Education Expenses

Veterans looking to invest in education or support their children’s educational pursuits can benefit from the funds obtained through a VA refinance loan. Whether pursuing a degree, vocational training, or assisting with tuition costs, this option offers a strategic means to access capital for educational endeavors.

Emergency Expenses

Life is unpredictable, and unexpected expenses can arise. VA cash-out refinance provides a safety net for veterans, allowing them to access funds in times of financial need. Having quick access to equity can be invaluable when facing medical emergencies, unforeseen home repairs, or other urgent situations.

Starting a Business

For entrepreneurial-minded veterans, using the funds from a cash out refinance loan to start or expand a business is a viable option. This financial infusion can provide the capital needed to pursue business ventures, creating opportunities for veterans to achieve economic independence.

Investments

Veterans with a keen interest in investments can leverage the released equity to diversify their portfolios. Whether investing in real estate, stocks, or other ventures, the ability to access funds through a VA cash out refinance loan opens up avenues for wealth-building and financial growth.

Veterans can strategically leverage their home equity to fund various endeavors, from improving their living spaces to consolidating debts, supporting educational pursuits, handling emergencies, exploring entrepreneurship, and engaging in investment opportunities.

Eligibility Requirements for VA Cash-Out Refinance

Ensuring a smooth and successful application process for VA cash-out refinance involves meeting specific eligibility criteria. Veterans must navigate through a set of requirements, covering factors such as creditworthiness, property valuation, and primary residence status.

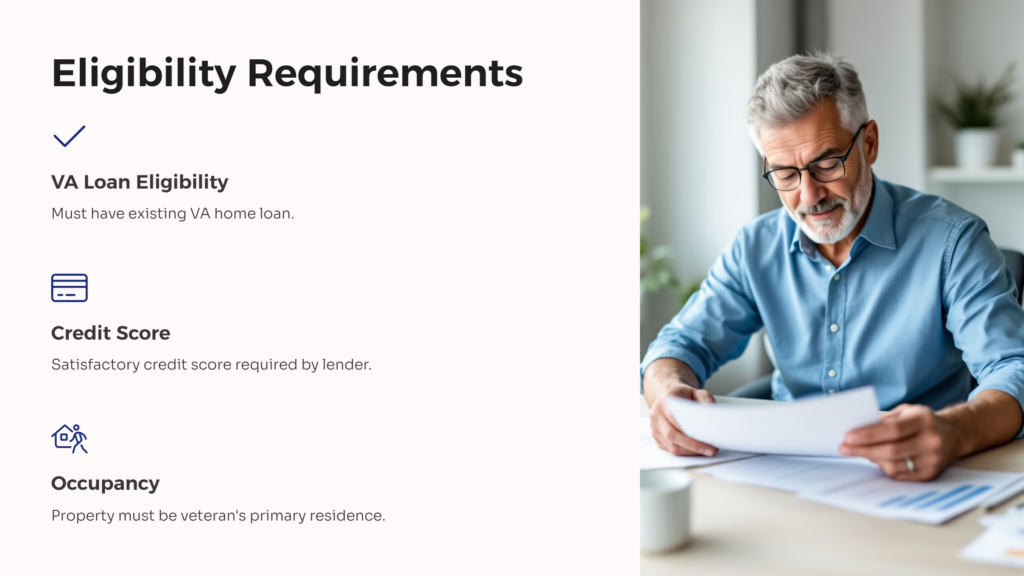

VA Loan Eligibility

The fundamental prerequisite for VA cash-out refinance is having existing VA home loans. Veterans should confirm their eligibility for a VA loan before proceeding with the cash-out refinance application.

Credit Score

While the VA itself does not set a minimum credit score requirement, the VA lender may have his own standards. Typically, a satisfactory credit score is preferred, demonstrating the borrower’s ability to manage financial responsibilities.

Loan-to-Value Ratio (LTV)

The Loan-to-Value ratio, or LTV, is a critical factor in determining eligibility. LTV represents the proportion of the new VA home loan amount to the appraised value of the home. VA guidelines often allow a maximum LTV of 90%, meaning veterans can refinance up to 90% of their home’s appraised value.

Occupancy Requirements

To qualify for VA cash-out refinance, the property being refinanced must serve as the veteran’s primary residence. This ensures that the financial benefits are directed towards the veteran’s housing needs and stability.

Veterans seeking to explore the benefits of VA cash-out refinance must familiarize themselves with the eligibility requirements. From confirming VA loan eligibility to understanding the significance of credit scores, Loan-to-Value ratios, and primary residence status, meeting these criteria is crucial. By doing so, veterans can position themselves for a successful loan estimate, ultimately unlocking the financial advantages of VA cash-out refinance.

The Process of Obtaining a VA Cash-Out Refinance Loan

Starting the process for a VA cash-out refinance is a smart move for veterans seeking financial benefits from their home equity. To make the most of this opportunity, veterans should understand the step-by-step process.

Initial Inquiry

The VA loan process begins with veterans expressing their interest and making an initial inquiry with a VA-approved lender. During this stage, lenders may provide essential information about the requirements, benefits, and potential terms associated with the cash-out refinance.

Confirming Eligibility

Veterans must confirm their eligibility for a VA cash-out refinance by meeting the necessary criteria, including having an existing VA home loan, maintaining a satisfactory credit score, and ensuring compliance with the Loan-to-Value ratio and occupancy requirements.

Document Gathering

The application process involves gathering and submitting the necessary documentation. This may include proof of income, tax returns, details about existing debts, and other financial records. Clear and accurate documentation is vital to expediting the underwriting process.

Property Appraisal

Lenders typically require a professional appraisal of the property to determine its current market value. This step is crucial in establishing the Loan-to-Value ratio, a key factor in determining the loan amount.

Loan Application Submission

Once all documentation is in order and eligibility is confirmed, veterans can formally submit their application for the VA cash-out refinance loan. This initiates the underwriting process, during which the lender assesses the borrower’s financial situation and the property’s value.

Loan Approval and Closing

Upon successful completion of underwriting, marking a significant milestone in the VA cash-out refinance journey, the lender issues loan approval. This approval signifies that the borrower meets the criteria, the property’s value aligns with expectations, and the terms of the new loan, including the VA funding fee, have been established.

The final step in the VA loan process is the closing. During this crucial phase, veterans have the opportunity to finalize the terms of the new loan and officially complete the transaction. Here, they sign the necessary paperwork, formally acknowledging their commitment to the new loan terms and the utilization of funds obtained through the cash-out refinance.

It’s important to highlight a key aspect associated with the closing process: Closing Costs. These are the additional expenses beyond the loan amount that borrowers may encounter when finalizing the loan transaction. Managing closing costs, including the VA funding fee, is an integral part of the overall financial strategy when pursuing a VA cash-out refinance.

Risks and Considerations

While VA cash-out refinance presents numerous advantages, it is essential for veterans to approach this financial tool with a clear understanding of potential risks and considerations.

As veterans explore the potential benefits of VA cash-out refinance, it’s crucial to be aware of the associated risks:

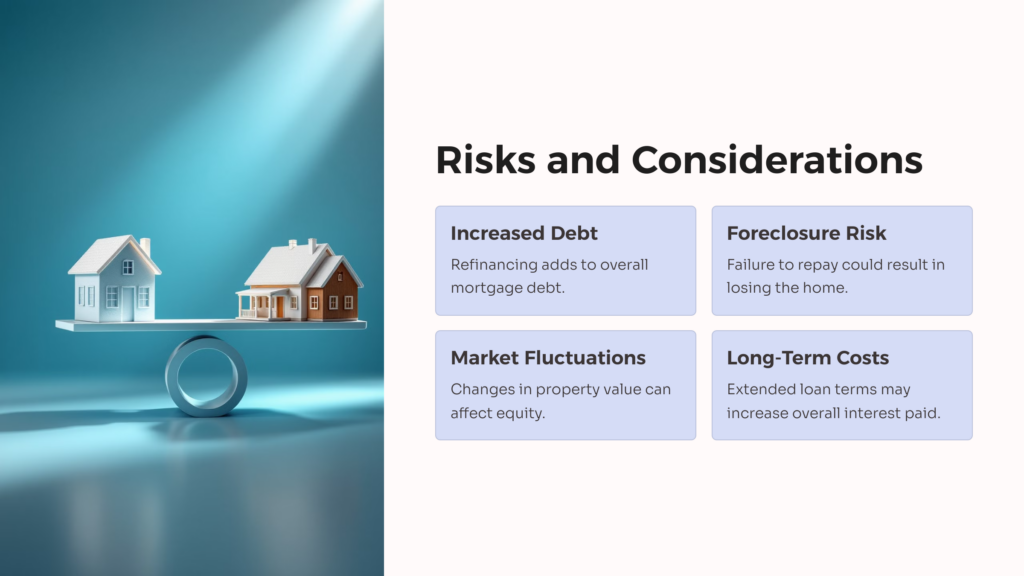

Increased Debt

One of the primary considerations is the potential for increased debt. By refinancing and pulling equity from their homes, veterans effectively add to their overall VA mortgage debt. Careful consideration must be given to the purpose of accessing these funds to ensure that the VA benefits outweigh the long-term financial impact.

Risk of Foreclosure

The risk of foreclosure is a significant concern, especially if veterans face difficulties in meeting the repayment obligations of the new, larger home loan. Failing to adhere to the terms of the cash-out refinance can put the veteran’s home at risk, emphasizing the importance of carefully assessing one’s financial capacity before proceeding.

Market Fluctuations

Home values can fluctuate based on market conditions. Veterans should be mindful of the potential impact of market changes on the equity in their homes, as it directly affects the Loan-to-Value ratio. A decline in property values could result in reduced equity and limit the benefits of the cash-out refinance.

Long-Term Interest Costs

While VA loans typically offer competitive interest rates, extending the loan term or increasing the loan amount can lead to higher long-term interest costs. Veterans should carefully evaluate the trade-offs between immediate financial needs and the overall cost of the loan over time.

Spending Discipline

Access to significant cash through a VA cash-out refinance requires discipline in managing those funds. Veterans must resist the temptation to use the funds impulsively, ensuring that the investment aligns with their financial goals.

While VA cash-out refinance offers valuable financial opportunities, it is not without its risks. Veterans must carefully weigh the potential drawbacks and considerations, ensuring that the decision aligns with their long-term financial goals and capacity.

Comparing VA Cash-Out Refinance to Other Financing Options

When exploring financing options, understanding the nuances between VA cash-out refinance and other choices is crucial. Each option comes with its own set of advantages and considerations, allowing veterans to tailor their financial decisions to align with their specific needs and circumstances.

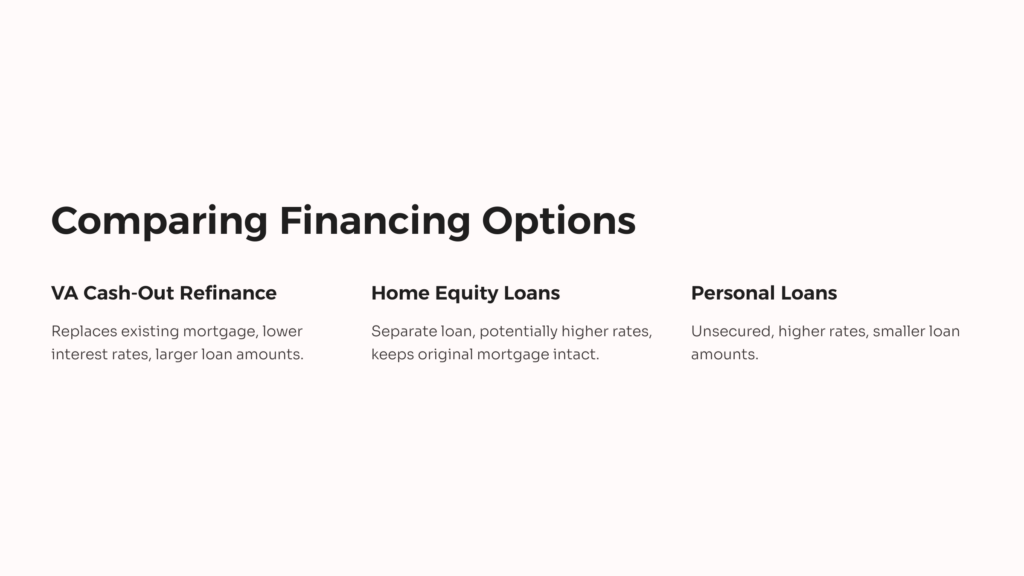

VA Cash-Out Refinance vs. Home Equity Loans:

- Collateral and Purpose: Both options leverage home equity as collateral, but while a VA cash-out refinance replaces the existing mortgage, a home equity loan is a separate loan with its own terms.

- Interest Rates: VA cash-out refinance often offers lower interest rates compared to a home equity loan, making it a potentially more cost-effective choice.

VA Cash-Out Refinance vs. Personal Loans

- Collateral and Amounts: VA cash-out refinance uses home equity as collateral, generally allowing for larger loan amounts than unsecured personal loans.

- Interest Rates: VA cash-out refinance tends to have lower interest rates due to the secured nature of the loan compared to the typically higher rates associated with personal loans.

VA Cash-Out Refinance vs. Credit Cards

- Interest Rates and Limits: VA cash-out refinance usually offers lower interest rates and allows for larger amounts compared to credit cards.

- Debt Consolidation: While both options can be used for debt consolidation, VA cash-out refinance provides a structured repayment plan compared to the revolving nature of credit card debt.

VA Cash-Out Refinance vs. Traditional Refinancing

- Access to Funds: Traditional refinancing aims to secure a lower interest rate, while VA cash-out refinance provides access to funds by increasing the loan amount.

- Use of Proceeds: VA cash-out refinance allows veterans to use the funds for various purposes, whereas traditional refinancing primarily focuses on improving loan terms.

Comparing VA cash-out refinance to alternative financing options provides veterans with a comprehensive understanding of the available choices. By evaluating the nuances of each option, veterans can strategically align their financial decisions with their immediate needs, risk tolerance, and long-term objectives. This thoughtful comparison empowers veterans to navigate the landscape of financial choices with confidence and optimization.

VA cash-out refinance stands as a valuable financial tool for veterans, offering access to funds with favorable terms. While it presents numerous benefits, it’s crucial for veterans to carefully consider their financial situation, weigh potential risks, and explore alternatives.

For veterans looking to explore the benefits of VA cash-out refinance further and make strategic financial decisions, check out our other blogs. At All Veteran, we support veterans on their journey to financial empowerment, providing valuable insights and personalized assistance. We can help you navigate the diverse landscape of financial choices.

AllVeteran.com Advisors

AllVeteran.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.