The VA Interest Rate Reduction Refinance Loan (IRRRL), or the VA Streamline Refinance, is a mortgage program specifically designed for Veterans who already have an existing VA home loan. It lets veterans refinance their current loan to potentially secure a lower interest rate, thus lowering the monthly payments. It will even allow a veteran to switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage for more stability. This streamlined process makes it faster and easier to refinance compared to traditional options.

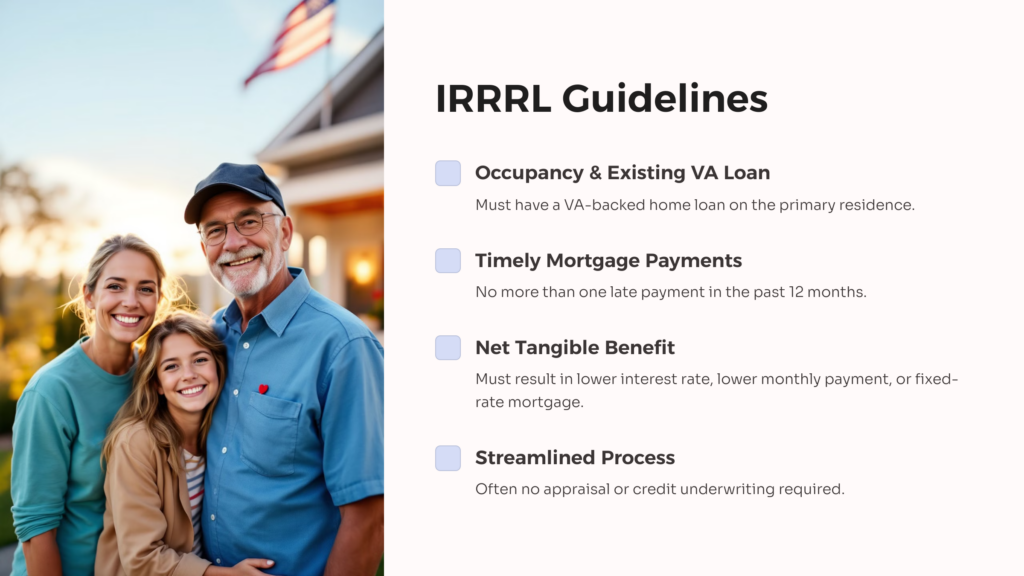

Guidelines

Occupancy & Existing VA Loan: The borrower must currently have a VA-backed home loan on the property being refinanced and ensure that is their primary residence.

Timely Mortgage Payments: A good payment history on the existing VA loan is important, as with any refinance. Ensure that there is no more than one late payment in the past 12 months to achieve desired results.

Net Tangible Benefit: The refinance must result in a tangible benefit to the borrower, meaning either a lower interest rate, a lower monthly payment, or a move from an adjustable-rate mortgage to a fixed-rate mortgage.

No Appraisal or Credit Underwriting: In many cases, an appraisal or credit underwriting may not be required, making the process more streamlined.

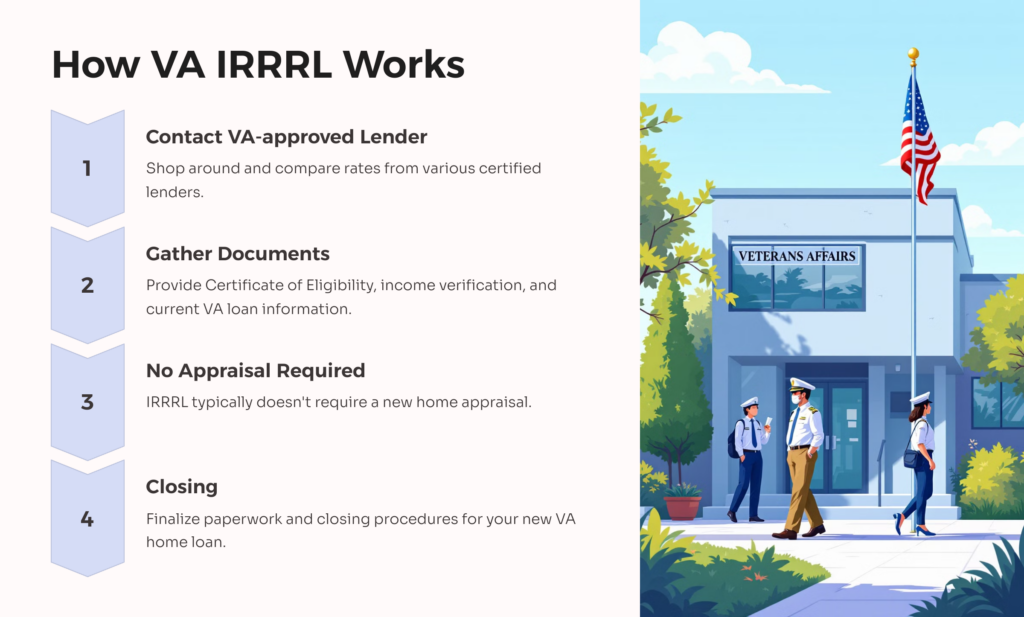

How does VA IRRRL work:

- Contact a VA-approved lender: Shop around and compare rates from various lenders such as a private bank, mortgage company, or credit union certified to offer VA loans. Terms and fees may vary by customer, so ensure to contact multiple lenders to review your options.

- Gather required documents: Provide paperwork like your Certificate of Eligibility (COE), income verification, and current VA loan information. If you don’t have your original COE, ask your VA lender to get your COE electronically through the VA Home Loan program portal.

- No appraisal: Unlike typical refinances, an IRRRL typically doesn’t require a new home appraisal.

- Closing: Once approved, finalize the paperwork and closing procedures for your new VA home loan.

Benefits of VA IRRRL for Veterans:

- Lower Interest Rates: If interest rates have fallen since you took out your original loan, you could lower your monthly payment significantly by refinancing to a new, lower rate.

- Reduced Payments: Small interest rate drops can result in substantial savings over the life of your loan, freeing up money for other expenses. Additionally, closing costs may be minimal or nonexistent.

- Switch to a Fixed Rate Mortgage: If you have an adjustable rate mortgage (ARM), an IRRRL is essential in converting your payments to a predictable fixed rate mortgage, protecting you from future interest rate hikes through the duration of your existing loan.

- Faster Process: Compared to traditional refinances, IRRRLs involve less paperwork and require no new appraisal, leading to a significantly quicker closing time.

- Minimal Credit Check: Unlike typical refinances, credit checks are often waived or less stringent with IRRRLs, making them an option for Veterans with less-than-perfect credit. In other words, a low credit score doesn’t exactly disqualify you from achieving this type of refinance.

Disadvantages of VA IRRRL for Veterans:

- No Cash-Out: It is important to note that IRRRLs are designed for refinance rate and term refinancing ONLY. Cash-out refinancing is not applicable with this instrument. This can be a major downside, particularly considering recent steep increases in equity for many as home values have risen. With an IRRRL, you won’t be able to tap into this equity to pay down debt, pay for home improvements or reach another financial goal.

- Interest Rate Cap: You will be ineligible for a streamline refinance if your new VA refinance rates are higher than your original rate.

- Funding Fee: The VA IRRRL has a 0.5 percent funding fee, but it can be included in the loan amount so as to avoid upfront expenses.

- Credit, Income, or Employment Verification (optional): Depending on the lender, your credit, income, and employment may be reviewed lightly or not at all.

Comparison with Traditional Refinance:

- VA Funding Fee: A one-time fee based on the loan amount helps offset the program’s cost to taxpayers.

- Closing Costs: You may be responsible for various closing costs such as origination fees, title insurance, and recording fees.

- Interest Rate: Remember, while you’re aiming for a lower loan estimate, compare different lenders and offers to ensure the overall package is beneficial.

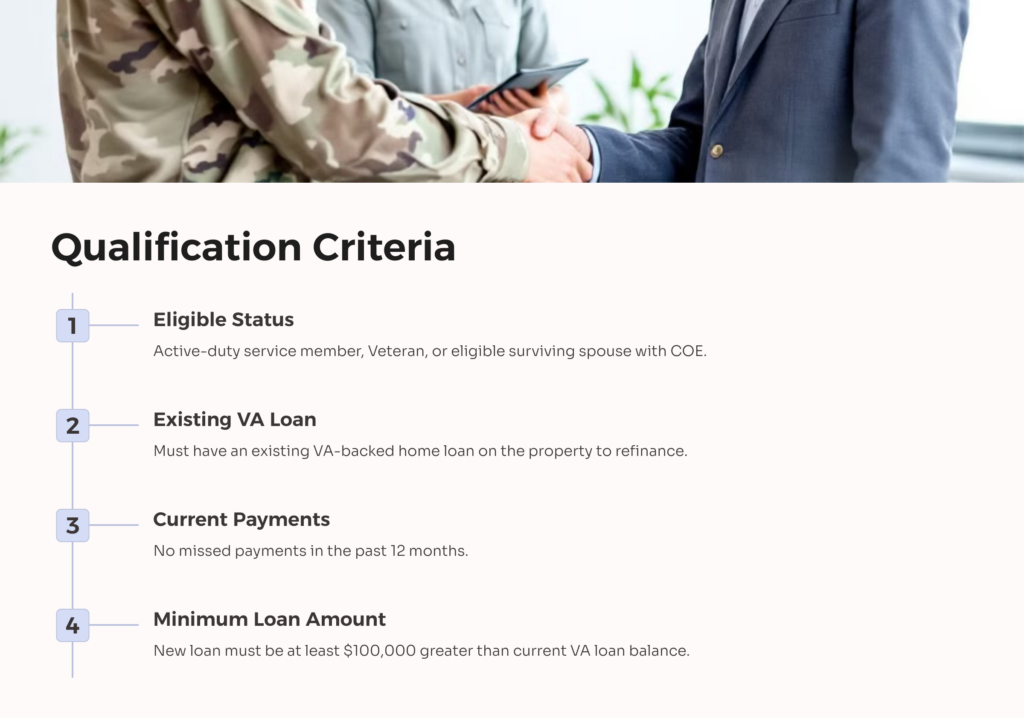

To qualify for a VA IRRRL, you must meet specific criteria:

- Active Duty, Veteran, or Eligible Surviving Spouse: You must be an active-duty service member, Veteran, or eligible surviving spouse with a Certificate of Eligibility (COE).

- Existing VA Loan: You must have an existing VA-backed home loan on the property you want to refinance. If there is a second mortgage on your home, it is necessary to have your mortgage lender agree to position your newly refinanced VA loan as the first mortgage.

- Current on Payments: You must be current on your mortgage payments with no missed payments in the past 12 months.

- Minimum Loan Amount: The new loan amount must be at least $100,000 greater than your current VA loan balance.

Documentation Requirements:

- VA Form 26-0285, VA Transmittal List.

- VA Form 26-0286, VA Loan Summary Sheet.

- VA Form 26-8320, Certificate of Eligibility.

- VA Form 26-8998, Acknowledgment of Receipt of Funding Fee from Mortgagee, or (if applicable)

- VA Form 26-0500, Notification to Mortgagee of Funding Fee Shortage to Mortgagee, or evidence borrower is exempt.

- Written Statement: signed veteran acknowledgment of the effect of the refinancing loan on the veteran’s existing loan payments and interest rate.

- Must Contain: the interest rate and monthly payments for the new loan versus that for the old loan.

- VA Form 26-8923, Interest Rate Reduction Refinancing Loan Worksheet.

- VA Form 26-1820, Report and Certification of Loan Disbursement.

- VA Form 26-8937, Verification of VA Benefit Related Indebtedness (if applicable).

- HUD-1 Settlement Statement (if applicable).

- VA Form 26-0503, Federal Collection Policy Notice.

- Any other necessary documents required by your VA lender.

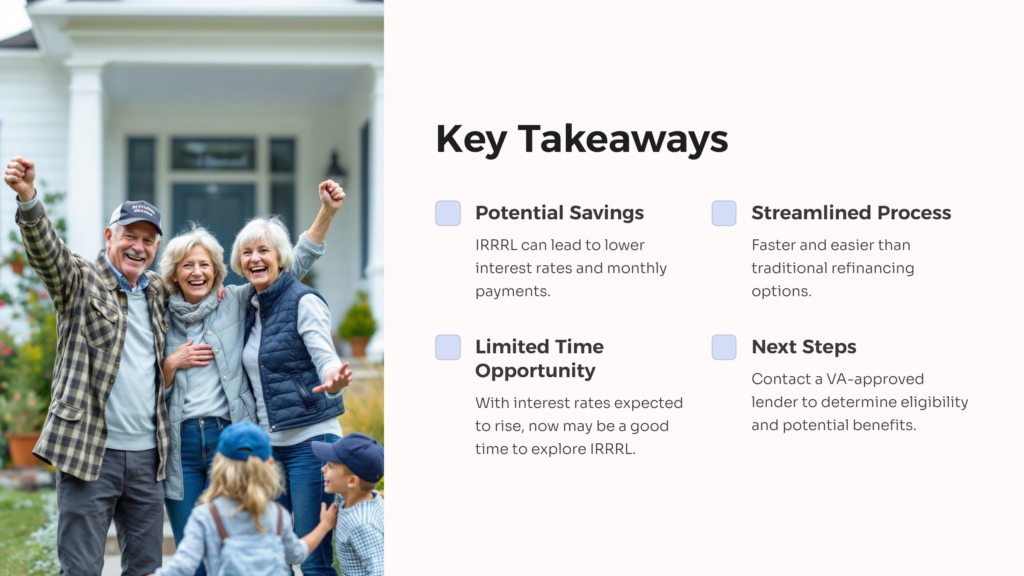

The VA Interest Rate Reduction Refinance Loan (IRRRL) program allows eligible veterans to refinance their existing loan at lower rates, providing potential monthly savings. By switching from adjustable-rate to fixed-rate mortgages, veterans can also gain more predictable housing payments. With interest rates expected to increase, now may be a good time for qualified veterans to explore refinancing through the IRRRL program. Contacting a VA-approved lender can help determine if you are eligible and could financially benefit.

AllVeteran.com Advisors

AllVeteran.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.