VA loans are a great financial tool designed to provide every eligible service member, veteran, and their spouses with attainable homeownership. They were established in 1944 as a part of the GI Bill of Rights—an initiative targeting veterans returning from World War II. The VA’s goal in lending is to keep housing affordable so that veterans can purchase properties.

VA loans offer some worthwhile benefits. Different types of loans provide unique advantages. VA loans also offer significantly lower loan rates than many traditional options, giving veterans a straightforward path toward homeownership.

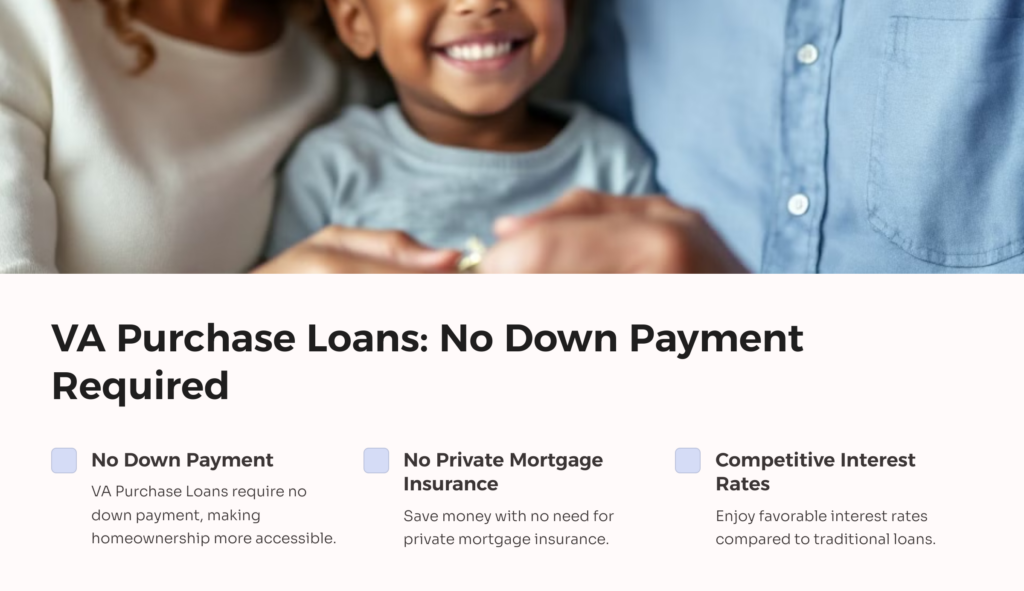

VA Purchase Loans

A VA Purchase Loan helps veterans and their families buy a home. One great thing about a purchase loan is that they require no down payments and no private mortgage insurance. They still offer competitive interest rates, though. To apply for a VA Purchase Loan, veterans need to get a VA home loan Certificate of Eligibility (COE), and contact a VA-approved lender. These easy steps will begin the VA loan process.

The COE confirms a veteran’s eligibility and states the maximum amount of VA home loan funding that a lender can provide them. To obtain your COE, you’ll need to submit a DD-214 discharge document or Statement of Service. These documents are for proving your qualifying military service. Veterans can apply either through their lender or by themselves. There are application options available via the VA website or by mail. The VA will review applications and mail eligible veterans their COE within 5-10 business days. The next step is for the veteran to meet with lenders who can provide income verification and discuss loan options. Lenders help facilitate the home-buying process, submit the loan request to VA underwriters, and handle loan closing procedures.

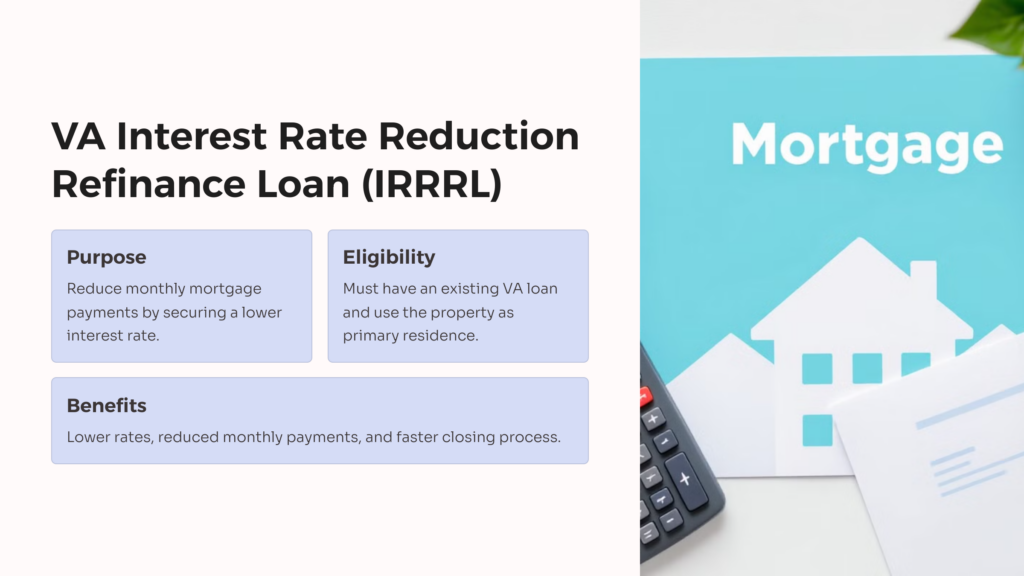

VA Interest Rate Reduction Refinance Loan (IRRRL)

Also known as the VA Streamline Refinance Loan, the VA Interest Rate Reduction Refinance Loan (IRRRL) aims to help homeowners reduce their monthly mortgage loan payments by securing a lower interest rate or transitioning from an adjustable-rate mortgage loan to a fixed-rate one. Eligibility requires having an existing VA loan and using the property as your primary residence.

Benefits from the IRRRL program include decreased VA loan rates, interest rates, lower monthly payments, and a faster closing process due to reduced paperwork. To apply for an IRRRL, homeowners should first discuss options with their lender, then apply via a VA-approved institution.

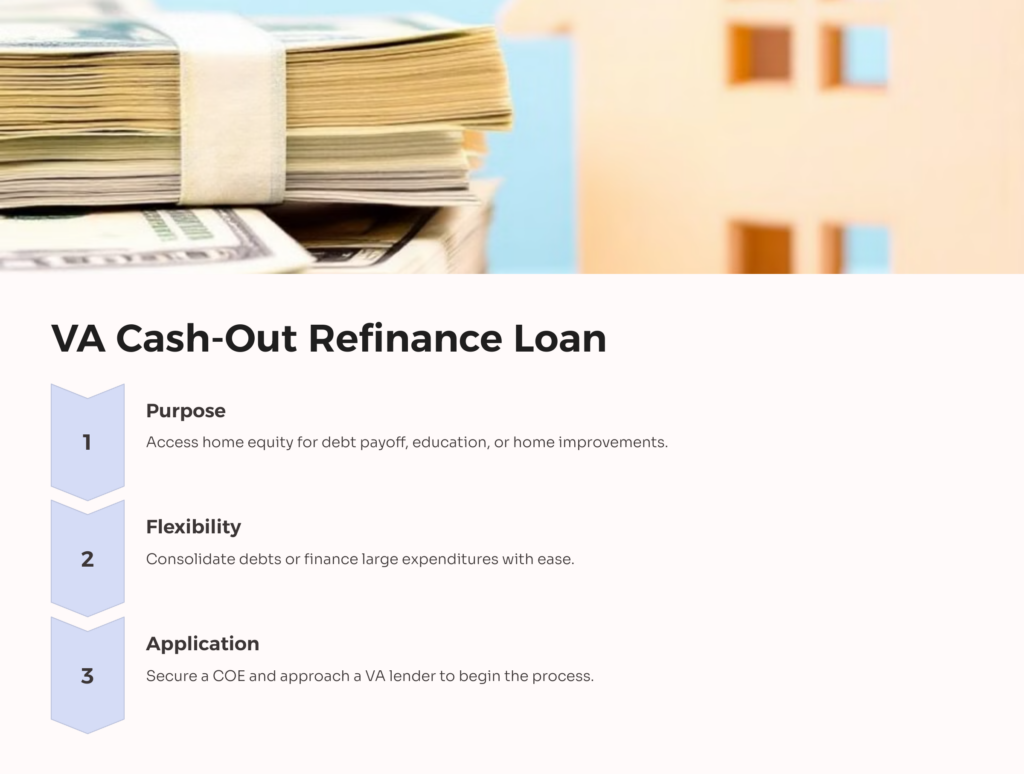

VA Cash-Out Refinance Loan

A VA Cash Out Refinance Loan is designed to enable veterans to take cash out from home equity to pay off debt, fund schools, or make home improvements. This loan type can also be used to refinance a non-VA loan into a VA loan. Eligibility is similar to a VA Purchase Loan, with veterans needing a COE.

The chief benefit of a VA Cash Out Refinance is its flexibility, as it allows veterans to consolidate their debts or finance large expenditures. To apply, veterans must once again secure a COE and then approach a VA lender.

VA Native American Direct Loan (NADL) Program

The VA Native American Direct Loan (NADL) Program provides support to Native American veterans and their spouses by offering direct home loans for purchasing, constructing, or improving homes on Federal Trust Land. Eligibility includes having a valid VA home loan COE, fulfilling income requirements, and intending to live in the home as your primary residence.

This loan option is a valuable option for Native American veterans. It offers low closing costs and requires no down payment. It also offers a fixed-rate 30-year loan term. Application for a NADL is simple, like most VA applications. Veterans must secure a COE and then apply directly through the VA.

VA-backed Energy Efficient Mortgage (EEM)

A VA-backed Energy Efficient Mortgage (EEM) enables homeowners to finance energy-efficient improvements on their homes. This includes solar heating and cooling systems, storm doors, and insulation. Eligibility requires a VA COE and acceptance of specific energy-efficient improvements.

The principal benefit of an EEM is the opportunity to finance energy-efficient improvements for up to $6,000 without needing a separate loan. The application process follows the same method as before; a VA lender must be sought after securing a VA COE.

Specialty VA Loan types

The VA offers specialized loan types. These include Adapted Housing Grants, which aid disabled veterans in purchasing, building, or modifying homes for improved livability. Supplemental loans are great helps for veterans in making home improvements and additions. The VA also offers a loan assumption feature, which allows eligible people to take over a VA loan from a VA borrower.

Regarding loan amounts, there is no national maximum limit to the amount a Veteran may borrow. The highest VA home loan amount available depends on the county loan limit where the home is located.

Veterans with full VA loan eligibility can borrow up to the county loan limit without a down payment. Those with partial eligibility may need to make a down payment to hit the max loan amount. Besides the county limits, veterans’ total borrowing power for a VA loan also depends on debt-to-income ratios, credit scores, and other factors impacting loan qualification.

VA Loan Life Insurance Rates

There’s a common myth that VA loan rates come with higher-than-normal life insurance rates. But in reality, life insurance rates are not directly linked to VA loans. Rates depend on factors such as age, health, and the amount of insurance required. Because VA loans are backed by the Department of Veterans Affairs, lenders see them as less risky. However, veterans who want life insurance must shop for separate policies. Life insurance companies determine premiums based mostly on an individual’s health, age, lifestyle habits like smoking, and the amount of coverage they request. They do not consider whether the policyholder has a VA home loan. So while VA borrowers enjoy favorable mortgage terms, they can expect to be assessed for life insurance individually like any other applicant.

AllVeteran.com Advisors

AllVeteran.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.